25 March 2026

|5 minutes

Understanding smoothed funds in changing market conditions

Introduction

Many investors are navigating a period of changing ISA rules, market volatility and rising awareness of the long‑term impact of inflation. As the Cash ISA allowance is set to reduce in 2027 following the 2025 Autumn Budget announcements, more investors and advisers may be reassessing the role that cash and investments play in meeting long‑term financial goals.

Smoothed funds - such as the Wesleyan Smoothed With Profits Growth Fund - aim to moderate the short‑term fluctuations of markets while remaining invested in long‑term growth assets. Smoothing does not remove investment risk, and the value of investments can still fall as well as rise, but the approach may help some investors feel more confident about remaining invested during periods of uncertainty.

To illustrate how different types of investors might think about these issues, we’ve created three conceptual, illustrative case studies below.

These examples are for educational purposes only and do not represent real customers. Suitability will always depend on an individual’s circumstances, goals, risk tolerance and capacity for loss.

Case study 1: The cautious, cash‑comfortable saver

Some ISA savers prefer the stability of holding cash, especially when they feel uneasy about market movements. However, for those with longer‑term goals, relying solely on cash may mean their savings do not keep pace with inflation.

In this conceptual example, "Fred" is a cautious saver who is particularly sensitive to short‑term fluctuations. While he values the perceived safety of cash, he also recognises that inflation may erode his spending power over time.

A smoothed fund may help reduce the appearance of day‑to‑day volatility while still investing in assets with the potential for long‑term growth. Smoothing does not eliminate investment risk, and the value of investments can fall as well as rise, but it may help certain cautious investors feel more comfortable with a long‑term investment approach.

This graph illustrates the type of short‑term variation that some investors find challenging. It is an example of the kind of market movement that smoothing seeks to moderate. This graph is for informational purposes only and should not be interpreted as a guide to future performance.

Case study 2: Supporting advisers with operational efficiency and client behaviour

Advisers frequently manage client assets across multiple platforms, where ISA allowances—typically up to £20,000 a year—represent only part of the wider portfolio. As a result, operational efficiency is an important factor in choosing suitable investment solutions. With the Wesleyan Smoothed With Profits Growth Fund now available on several mainstream platforms, advisers may find it easier to incorporate smoothing alongside other platform‑based investments where appropriate.

Beyond operational considerations, many advisers also face behavioural challenges with clients who react strongly to market movements or media headlines. These reactions can sometimes lead to impulsive decisions, such as disinvesting during periods of volatility, which may be detrimental to long‑term outcomes.

A smoothed fund does not remove investment risk, and values can still fall, but smoothing may help moderate the impact of short‑term market movements. This can support clients who may otherwise feel compelled to move into cash when volatility increases.

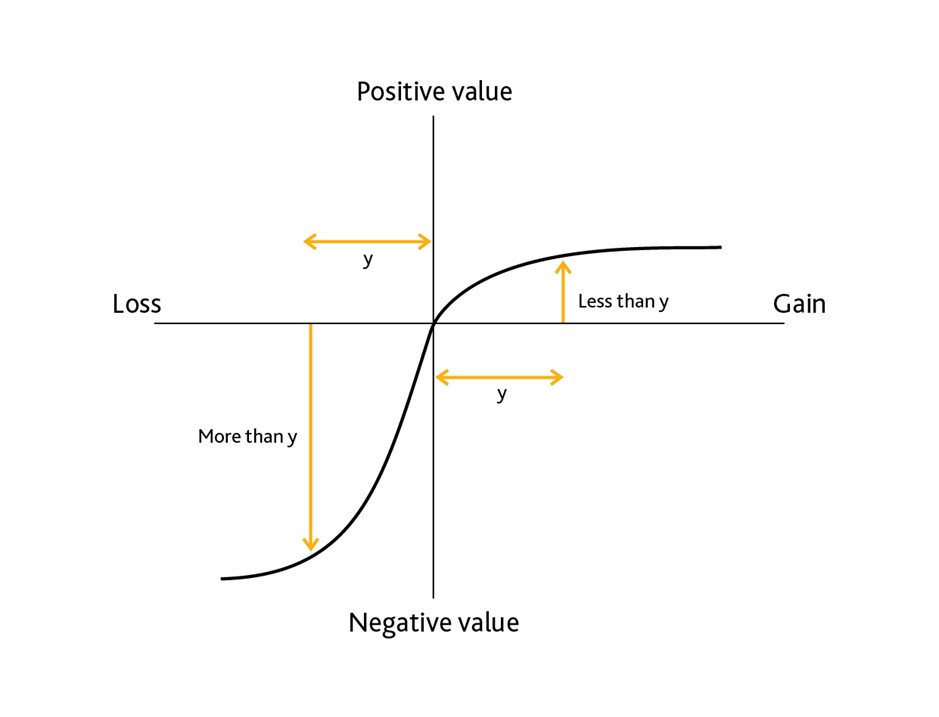

To illustrate the behavioural aspect of investing, the graph below shows how individuals often experience the pain of losses more intensely than the joy of gains — a well‑documented concept known as loss aversion. This psychological bias can make short‑term volatility feel more uncomfortable, contributing to decision‑making that may not align with long‑term goals.

This graph is for educational and behavioural‑insight purposes only. It does not represent fund performance or predict future outcomes.

Case study 3: Clients taking income and managing sequencing risk

For investors withdrawing income from their ISA - whether to supplement retirement income or meet shorter‑term financial needs - sequencing risk is a key consideration. This refers to the risk that a market downturn early in the withdrawal period can significantly reduce how long the investment lasts.

In this conceptual example, an investor draws regular income from their ISA under two approaches:

- remaining fully exposed to market volatility, or

- using a smoothed fund that aims to moderate the extent of short‑term fluctuations.

While both approaches still involve investment risk, smoothing may help reduce the immediate impact of downturns, supporting more stable withdrawals over time. This may be particularly relevant for long‑term income‑taking strategies, where longevity risk - the risk of running out of money - can also be a concern.

It is important to note that smoothing does not guarantee outcomes and will not protect against losses. Returns will vary depending on market conditions, the investor’s withdrawal pattern and the underlying assets in the fund.

How smoothed funds may fit into a wider investment strategy

Smoothed funds may be considered by:

- Cautious investors seeking a moderated investment experience

- Clients likely to react strongly to market headlines

- ISA investors reconsidering large cash holdings due to inflation or changing allowances

- Those taking regular income who may be exposed to sequencing risk

However, the suitability of a smoothed fund depends on several factors, including the investor’s goals, risk tolerance and financial position. Advice from a qualified financial adviser is essential.

The value of investments can go down as well as up, and investors may get back less than they invested. Past performance is not a reliable guide to future returns.

Smoothing does not eliminate investment risk or guarantee outcomes.

Tax treatment depends on individual circumstances and may change in the future.

The case studies on this page are conceptual and for illustrative purposes only.